Ship Science & Technology - Vol. 15 - n.° 29 - (71-88) July 2021 - Cartagena (Colombia)

https://doi.org/10.25043/19098642.226

Raúl E. Podetti 1

1 Vector Naval - Facultad de Ingeniería, Universidad de Buenos Aires. Buenos Aires, Argentina. Email: podettiraul@gmail.com

Date Received: August 28th, 2021 - Fecha de recepción: 28 de agosto del 2021

Date Accepted: November 25th, 2021 - Fecha de aceptación: 25 de noviembre del 2021

After an introduction on the region's shipbuilding industry, it moves into an analysis of some aspects of this industry's competitiveness, comparing Latin American (LatAm) shipyards with those of other regions with more developed industries. Among the m se aspects are: productivity, learning curve, specialization, labor cost, delivery times and government policies.

Second part deals with specific opportunities for domestic shipyards and ideas for developing their competitive advantages to generate value and social impact in the region, while safeguarding the environment. Six niches or opportunities are presented here, which are in all cases related to castinga new regard on Nature in our region. Nature being understood as the sum of natural resources, with the riches in fishery and offshore hydrocarbons standing out among them, but also those of the broad navigable rivers and lastly that of a privileged geographical position in terms of the extreme closeness to the Antarctic.

Key words: Shipyards, shipbuilding competitive factors, LATAM shipbuilding industry.

Tras una introducción sobre la industria naval regional se avanza en analizar algunos aspectos de la competitividad de esta industria, haciendo comparaciones de astilleros latinoamericanos con los de otras regiones con industrias más desarrolladas.

Luego se presentan algunas oportunidades específicas de los astilleros latinoamericanos e ideas de cómo desarrollar las ventajas competitivas para generar valor e impacto social en la región, cuidando el ambiente. Estos seis nichos se relacionan con el uso de los recursos naturales entendidos en sentido amplio, incluyendo riqueza ictícola, hidrocarburos costa afuera, disponibilidad de grandes ríos navegables y cercanía a la Antártida.

Palabras claves: Astilleros, factores de competitividad industrial naval, industria naval latinoamericana

In order to present specific opportunities of development, six niches are analyzed where competitive advantages are found for LatAm shipyards.

The work is manly focused on new ship construction and is part of major research effort that will be presented in a future publication Shipbuilding in Latin America, 100 years (1970-2070).

As a basic simplification it's possible to differentiate two large groups (hemispheres) of countries of the region: those of the Pacific + Caribbean and those of the Atlantic.

The maritime industries of the Pacific hemisphere are characterized by being led by state-owned shipyards, connected to their Navies even if their output isn't exclusively military. Such are the cases of ASMAR in Chile, SIMA in Peru, ASTINAVE in Ecuador, COTECMAR in Colombia and DIANCA in Venezuela, among others. Another characteristic of this group is an overall trend of slow but continuous growth without major upheavals, and their relatively higher share of shiprepair activities.

The Atlantic region, for its part, is practically the opposite. It is marked by the preponderance of private shipyards, by a higher relative participation in new constructions and by their characteristic cycles of bonanza followed by times of profound crisis mainly related to changing government industrial policies. This side of the continent exhibits the largest volumes of shipbuilding output, led by a vast margin by Brazil, the shipbuilding industry of which is by itself several times higher than that of the all the rest of Latin American countries put together. Ranking second in size is the case of Argentina despite the fact that it has already spent three decades of stagnation forced by the worst imaginable public policies. Also, to be mentioned are the cases of Paraguay with a growing development of "brown water" constructions and of Uruguay at a much more incipient stage.

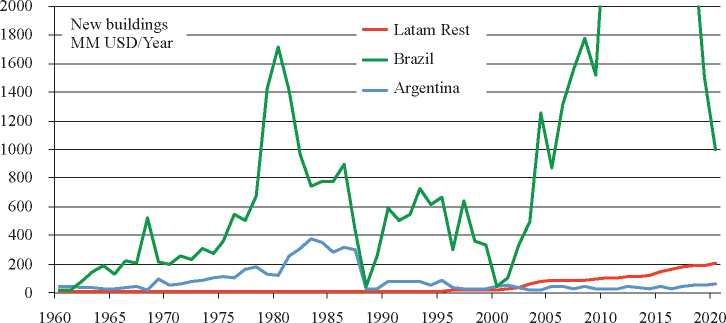

In Fig.1, a Timeline graph presents the Value evolution of the ship new building of Brazil, Argentina and the Rest of LatAm. This last one is based on gross estimates and it is steadily growing in this century mainly due to the output of Chile, Colombia and Paraguay.

Fig. 1. Shipbuilding Development in Brazil, Argentina and Rest of LATAM.

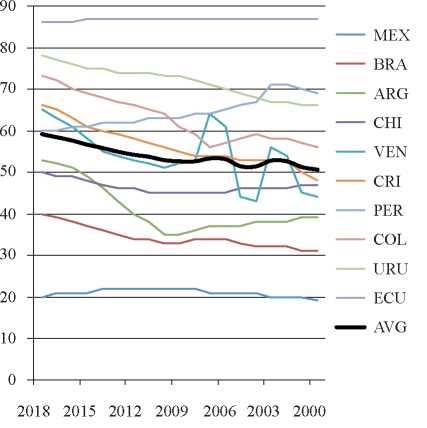

It is a fact that shipbuilding is not isolated from the rest of the country economic environment and that ships are capital goods that are traded at the international market. For that reason, it is interesting to have a look at LatAm countries competitive ranking position in the global arena. This is presented by the United Nations Industrial Development Organization (UNIDO) who develops the Competitive Industrial Performance Index (CIP). The relevance of this index to the competitiveness of ship building industries is demonstrated by realizing that over 90% of global ship production is concentrated in the top seven countries of the CIP 2010[10] ranking (Japan, Germany, USA, Korea, Taiwan, Singapore and China). But in CIP 2018 this concentration increases even more (top 4 countries). In the region, the top four industrially competitive countries in 2010 were Mexico, Brazil, Argentina and Chile. Taken together, Brazil, Mexico and Argentina accounted for 4.2% of world manufacturing value added and 3.7% of world manufactures trade.

Among the 133 countries considered, the top ten LatAm performers are presented in Fig.2, confirming a fairly stable ranking positionduring the first decade of the century, but they decline in the second decade. LatAm countries have lost positions, making more difficult to compete internationally with industrialized goods as ships.

Fig. 2. Top 10 LatAm International Industrial Competitiveness Ranking.

When analyzing the different aspects of competitiveness, it is possible to identify several "external" factors, beyond the control of a shipyard's management. Meanwhile, "internal" factors, which can be controlled by industry executives, constitute its "intrinsic competitiveness." As industrial economic entities, shipyards seek to grow competitively to better achieve the objectives of their shareholders, who can be private or governmental. This aspect leads us to one of the first issues to the analyzed and which is, precisely, the difference between state-owned and private shipyards, since both exist in LatAm.

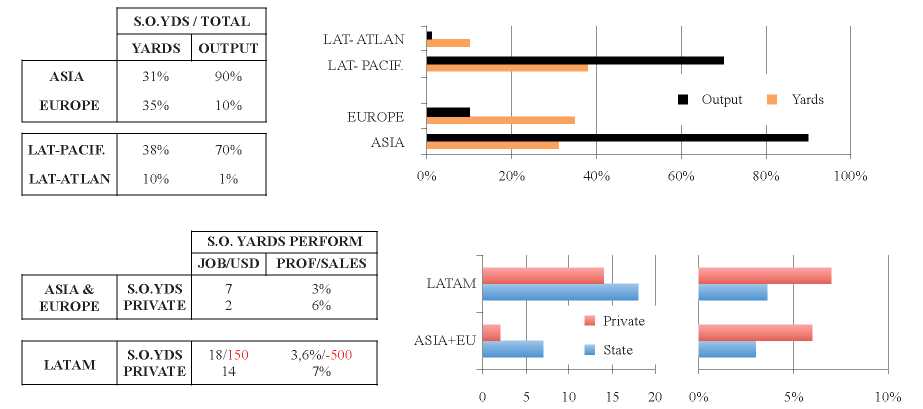

A recent study [6] which presents the relative importance of state-owned shipyards in different regions is combined with the LatAm case [7], showing, in Fig.3, the market share of State-owned shipyards, their ratio of profit and employees to sales (in millions of dollars). As the argentine state-owned yards have a very poor average performance (in rednumbers) they cannot even be shown in the graphs.

Fig. 3.State Owned Shipyards performance in LatAm and the World.

The above-mentioned study concludes that, in general, state-run shipyards are less efficient and flexible than private ones, making them intrinsically less competitive, and that the state-owned ones analyzed between 2012 and 2017 had an Employee/Sales ratio of twice that of private shipyards, that being one of the most widely accepted parameters of lack of intrinsic competitiveness.

Lastly the OECD study mentions that the decisions taken by state-owned shipyards tend to be more closely related to political and electoral purposes than to criteria of industrial competitiveness, and refers to situations of disloyal competition between governmental shipyards and their private peers at national and international level. In the Argentine case there are several situations of this kind inits shipbuilding history, and in the Chilean case this constitutes one of the complaints of industry, according to a published survey [5].

When comparing the performance of Argentine state yards with similar ones (ASMAR, COTECMAR, SIMA) throughout the region, it is found that in Argentina overstaffing is significant, productivity (Employment/MMUsd) is much worse, and structural losses have remained unresolved for decades, mainly in Rio Santiago shipyard.

The most customary index for measuring this (for sizable ships) is the amount of Compensated Gross Tonnage (CGT) produced in relation of the unit of Man-Hours (MH) worked. The best levels attained in LatAm was at Brazilian yards, prior to the crisis of the 1990s, and were of the order of 65 MH/CGT and the average stood at 85, while Korean shipyards stood (1992) at 45 [9]. But for medium and small size ships that are the vast majority in LATAM case, the parameter of MH/CGT is not the most adequate, and given the different type of vessels built a better parameter would be Jobs/MMusd of production value.

Fig.4 [7] shows the cases of more than 95% of world production on three continents. Brazil and Argentina (private shipyards) exhibit similar ratios, in the order of 21 jobs per million dollars of production, as do those of Latin America's principal Pacific shipyards, showing that, in comparison with other regions, there is still much room for improvement.

Fig. 4.Shipyard Productivity (Employee/Value).

In Mexico [3] the average ratio for 2009 and 2014 was much higher, in the order of 47 Jobs/MMusd. One reason for the curves to tend downwards is the global trend to external subcontracting, keeping only the most essential tasks concentrated in shipyards, like assembly, project management, final outfitting, testing, launching and site management.

International studies [4] show much lower values for high production regions: Values for Japan and Europe are close to 6 jobs/MMUsd, South Korea,4 and China, 10.

Shipbuilding industry is characterized by a slow product innovation, so that advantages are achieved via continuous process improvements over the course of time, through learning. The concept of "continuity" needs to be stressed, for the positive effects of the learning to be really effective. In the cases of Korea and Japan, their current very high levels of productivity are mainly due to thirty years of continuous shipbuilding activity. In the case of LatAm, the larger shipbuilders (Braziland Argentina) have never managed to maintain continuity for more than 15 years. This is not the case on the LatAm Pacific hemisphere where yards have enjoyed longer periods of continuous work but at a smaller scale.

Improvement depends on the position of shipyards on their learning curve. Brazil stood (2012) with a factor of 85% [9]. This means that for every doubling of cumulative production, the improvement in productivity would be of 15% in terms of MH/CGT. For comparison purposes, the Asian countries that are most advanced on the curve stand at a factor of 70%.

Continuity is one of the most important factors to attain higher levels of competitiveness for the previous reasons and others as will be seen later on.

Shipyards achieve higher competitiveness when they carry out repetitive construction.

Brazilian yards have begun to specialize but without sufficient repetitions. A case of success[2] was the Brazilian yard Wilson & Sons that expanded, investing in technology to specialize in the Offshore Support Vessels niche. In Argentina and Paraguay there are good examples in the barge building niche. But, again, the lack of continuity due to bad government policies stopped these developments, destroying the value generated.

The labor cost at a Brazilian yard, working regularly in a continuous manner in the 1985-1996 period was of between 40% and 60% of the Japanese cost and between 50% and 70% of Korea's.

That same study explains that labor share in total cost strongly depends on the wage level and labor intensity of the process. In Europe and Japan may vary from 23% to 50%, in Korea are close to 19% and in India may be as low as 8% of total shipbuilding cost. As a general value [4], it is concluded that over half of the costs are equipment and materials (55% to 65%) and the rest is labor, services and overhead.

An analysis dated 1999 shows that total costs in Brazil for local yards were 40% higher than the best international ones, but were only 5% above international ones as regards their export, by reason of the lower applicable taxes and lower demands for the use of local marine parts which were more expensive.

Studies in 2013 show that the price of steel accounts for 20%/30% of the cost and that Brazil has been efficient as regards that output. Labor represents between 15% and 20% of the cost of ships, and equipment is 30% to 50% of cost.

The average delivery time of Brazil's five largest shipyards between the years 1983 and 1996 was of 68 months, but that period was marked by several crises with production discontinuities. The case of Ishibras, between 1990 and 1994, is more realistic since it operated in a continuous manner on a series of eight Suezmax oil tankers for export with anaverage delivery time of 82 weeks, which can stand comparison with timeframes in Korea (27 weeks) and Europe (66 weeks). That was the Brazilian best performance.

Barge building in Argentina and Paraguay have reached very short delivery times in a series production system (as low as one 2500dwt bargeper week at SANYM yard in year 2000) but still far from US yards output of on 1500 dwt bargeper day.

Many countries consider the maritime industry as strategic, for which reason they generate protection mechanisms that guarantee its existence. A 2001 study by UNCTAD [1] identifies 17 types of maritime subsidies, and the countries that apply them. These policies are mainly in support of shipping lines and several are also, indirectly, an incentive to shipyards. Brazil is located in an intermediate position, applying 41% of the policies in 2001, in the following years in creasing this both in number and in magnitude of application. At the same time, more than 60% of countries with a maritime industry apply the following policies: Coastal Traffic Reservation, Bilateral Agreements, Tax Reductions, Financing Programs and Subsidies.

Experience indicates that promoting the supplying of the domestic market is a good way of achieving sectorial development. But it is also markedly important to seek technological development, increases in productivity and the development of suppliers, since only those that are internationally competitive will thrive when, for some reason, the protections are reduced.

Korea and Japan are recent successful examples of industries that were strongly protected and promoted over a period of time and that gradually generated such competitiveness that it allowed them to continue to compete after the subsidies were reduced. In any event their governments follow developments attentively and act in their defense in crisis situations.

Never theless, competitiveness must not be sought at any price. Policies must, whenever possible, be created without cross subsidization such that other industries finance the shipyards or ship owners. Although subsidies are frequently necessary at moments in which an industry is recovering, they must be transitory and be gradually reduced.

In Colombia the programs AntiTrámite and ProAstillero are very positive actions towards eliminating productivity barriers, as well as there cent decree 1156/2020 that eliminates import duties on 350 items of parts required to build shipsin Colombia.

Shipbuilding is cyclical and continuity is key to competitiveness. Therefore, it is expected that governments will take action to protect the high valued competitiveness attained by their respective shipyards when a crisis arises.

In LatAm we have basically two very different attitudes: In Brazil and Argentina, government shave suspended all kinds of supports during low cycles, worsening the crisis and losing all the competitive edges developed. In the Pacific hemisphere, governments keep supporting (at least at a minimum level) the state-owned yards during critical times, thus permitting them to keep building productivity.

In the rest of the world, some of the actions to support the shipbuilding industries during 2007 crisis were [4] the following: Korea announced 18 billion Euros support package to shipyards and the ExImBank put aside 8,5 trillion won for loans to small yards and encourage private banks to facilitate guarantees for ship export operations. The “Buildin India Policy” was launched with large fundingand 30% subsidies for orders placed before August 2007 and 20% for those placed onwards. USA put a special stimulus package with a large budget to acquire a fleet of public service vessels, suchas ferries. The “Build in Turkey Policy” offered extended facilities for ship exports and provided financial support for shipyards in trouble.

It is unrealistic to expect LatAm shipyards to be competitive in all type of vessels. Therefore, it iswise to identify the most convenient niches and concentrate in them.

Both the South Atlantic, close to Uruguay and Argentina, and the South and Central Pacific alongside Chile, Peru, Ecuador, Colombia, Mexico and Central America, are among the richest fishing grounds at worldwide level, and coastal nations have an ample tradition of fishing activities and construction of fishing vessels. Nevertheless, the majority of larger-sized fishing vessels are imported, and local industries must settle for building smaller crafts, as if it weren't possible to build them competitively in each country, orat least at regional level. This is clearly the result of bad state public policies, across the continent, which in many cases answer to a combination of lack of information, indifference and corruption. Argentina's fisheries case is paradigmatic. Despite having a large maritime construction capacity, more than half of its fishing vessels have been imported second hand and tax-free, representing 85% of current hold capacity [7]. The last fifteen Argentine governments expedited the free importation of second hand fishing vessels larger than 40 m in length, arguing that they couldn't be built in Argentina, even as domestic shipyards were delivering larger and more complex ships for local and export markets.

The fishing nations par excellence (Spain, Japan, Korea and China) dump their played-out ships in these underdeveloped fisheries and thus modernize their own fleets; and additionally position their own firms to thus ensure control over these key natural resources.

Without going into the political debate on the best way to exploit each country's oceanic resources, what is indeed clear is that our governments should prioritize local ship construction. If shipyards weren't prepared for it, foreign firms could be incentivized to set themselves up and build the ships locally. And in those countries where the industrial capacity does exist, agreements could be generated for foreign companies to contribute all the imported equipment for building the vessels locally.

This natural wealth that belongs to all of us inhabitants of each fishing nation needs to be shared out better, among us, the owners of the resources. One way to do it is precisely by promoting the domestic construction of the ships involved. Andin this process, we will in addition, be doing it with ever rising competitiveness — something that will never be achieved if we import what we are able tobuild. This is undoubtedly an opportunity niche for increasing in competitiveness.

As with the case of the fisheries resource, that of offshore oil and gas should be regarded as an opportunity for the development of the owners ofthis resource, who are neither governments nor oil companies, but the current and future inhabitants. And one of the fastest and most profound ways of achieving this is through construction of the support vessels, platforms and ships for this activity with rising levels of domestic content.

The case of offshore in Brazil is exemplary for understanding the transformative capacity of the marine industry, which took employment at the shipyards from 2,000 workers at the turn of the century, to some 80,000 a decade later. But for this to happen there was a state policy strongly maintained over time [8].

Brazil convinced the world's largest builders of offshore structures and vessels to associate with domestic companies and produce as much as possible in Brazil, contributing capital and technology. The results were amazing and the first signs of rising competitiveness began toarise especially in the construction of offshore support vessels, but the oil crisis and the cases of corruption at Petrobras blocked the effort — which, nevertheless, left its mark and much acquired knowledge, making it possible to aim at Brazilian exports for an offshore African development exhibiting similarities.

This is likewise an opportunity niche for the incipient offshore oil and gas production of Chile and Argentina and the more advanced ones in the rest of Latin America. Certainly, with a lower potential than Brazil, but, over the course of time, a rising presence of our shipyards in this sector will allow us to enjoy a clear competitive development.

As was mentioned above with regard to fishing activities, our Latin American seas contain great wealth. It's not in vain that pirate fishing fleets prowl around them in never-ending fashion.

Many Latin American countries began to take this path of domestic construction, increasing in experience and competitiveness. The best exampleis Chile's with its large series of locally built OPVs. But it is likewise the case of Peru, Ecuador, Colombia, Mexico and Brazil, which contribute 76% of regional content to the area's patrol fleets. Colombia stand out as their new OPV are Colombian designs. On the opposite extreme is Argentina that illegally imported a series of four OPV that could have been built locally.

This is a path that must not be given up and that should, rather, be strengthened, driving off the voices in alien languages that speak into the ears ofour Navy officers and Defense officials attempting to convince them that their own people are unable to build OPV.

In actual fact the solution could be Solomonic. We should split it down the middle. We will import (in soft financing terms) from one concentrated international source the package of equipment that we still don't manufacture (which represents approximately 50%), with the condition that this (exporter) country also finances us the other 50% of the construction that we'll carry out in our countries. They will have a negative initial reaction, but they will quickly realize that other countries are starting to negotiate in these new terms and a new competition game will be starting, not for 100% ofthe vessels' value but for the most profitable 50% (equipment, technology and systems).

Another natural resource at our disposal is constituted by our rivers. The intensive use of Latin America's broad interior hydric basins is a key to achieving competitiveness regarding the output of the continent's interior, output which because of its low unit value requires systems of transport in bulk at very low cost. Such is the case of convoys formed by a series of shallow-draft barges and pusher. These convoys can be built, with high levels of competitiveness, at the shipyards of Argentina, Brazil, Colombia and Paraguay.

These are the type of vessels located on the lowest rungs of the scale of shipmaking complexity, and their real and virtually sole challenge is to produce them at low cost — which is in turn relatively easy to achieve when enjoying medium to longterm horizons, in order for the investments to berepaid and the effects of the learning curve to be maximized.

In this sense, one may turn to the case of the U.S. and its gigantic inland fleet, which enables transport on the Mississippi River to contribute maximum competitiveness to the output of the interior of that country under the protection of the centenarian Jones Act, which provides the maximum imaginable market protection.

Argentina and Paraguay had begun to attain very high productivity levels until the worst governmental decisions halted it, favoring the tax-free importation of secondhand vessels (junk) and killing off all the competitive achievements that had been reached.

Added to the above-mentioned flow of bulk products that arrive by river at the large export ports are many others that come by train or truck to be loaded onto gigantic bulk carriers with worldwide destinations. In the face of this situation, the immediate temptation is to hope to have those large ships, or a majority of them, built at domestic shipyards. Although at one time they were indeed built at Brazilian and Argentine shipyards, and some could undoubtedly be manufactured today, everything indicates that the chances of doing so competitively are virtually nil. This is because the large shipyards of the East outdistance us sidereally in this type of vessels and it wouldn't be a good allocation of scarce resources to attempt to compete in that market. It is better to set aside the resources for the niches with a greater probability of success.

Nevertheless, if we take a detailed look at the operation of those large bulk carriers, we shall find other opportunities. Such are the cases of the tugs that assist them in port maneuvers, or the buoy setters that mark off the access channels to the ports, or, lastly, the powerful dredgers that deepen, widen and maintain the channels for those bulk carriers to be able to leave with the maximum possible load and thus cause the incidence of freight to be lower and our products to gain in competitiveness.

There is no doubt that Chile and Argentina's geographical position, closer than any other country in the world to the Antarctic continent, puts them in a privileged competitive situation for providing Antarctic logistics services related to the maritime industry, such as maritime maintenance and repairs first and construction secondly.

In order to increase the competitive advantage as regards repairs it's necessary to have workshops and maritime repair shipyards at the southernmost ports such as those of Ushuaia and Punta Arenas. It must be understood that these services followan export orientation, since the potential demand originates mainly from international fleets. These capabilities would also service the merchant vessels, fishing activities, the offshore activity off Tierra del Fuego and in the Strait of Magellan, and the increasing flow of cruisers.

As regards the ship construction of polar vessels both countries have had attractive experiences. In the case of Argentina, in addition to the construction of a polar ship in the 1980s, it has just concluded one of the world's most advanced polar projects with the modernization of the ARA Almirante Irízar icebreaker and there is a criticized project for the construction of a new polar vessel. In the case of Chile, marked progress is to benoted in the project of building a new icebreaker, which would be the first to be built in the southern hemisphere. At the same time, the Brazilian Navy has been holding talks with that of Chile fortheir participation in the construction of a new icebreaker for Brazil.

Only six market niches have been mentioned but there undoubtedly many other opportunities for competitive growth which it would be necessary to analyze. Among them could be that of coastal maritime transport; that of some vessels for defense; those of tourism activities, research work, shortdistance passenger transport, and pilotage services. A very special attention shall be paid in LATAM shipyards to the huge market opportunities that is unfolding due to the impact in shipbuilding and ship conversions due to Climate Change urgencies.

It is concluded that competitiveness, for the type of vessels which the Latin American shipbuilding industry can realistically aim for (niches), must be analyzed not only at the level of the region or country but also at that of the shipyards. Increasingly, equipment, materials and technology are be coming commodities available to all at virtually the same international price. What makes a difference is the intrinsic productivity achieved within the country, and mostly, at shipyard level including its subcontractors. Nevertheless, whatever the efforts carried out at industrial management level, without an adequate governmental policy that generates a competitive environment and ensures horizons of continuity, generating temporary protections appropriate for facilitating development, it will bedifficult to attain the levels of competitiveness that are needed in order to supply domestic markets, and especially to go out into the world exports market, which is what must really be aimed at to grow in volume and test competitive muscle.

AGÊNCIA BRASILEIRA DE DESENVOLVIMENTO INDUSTRIAL(ABDI) — Construção Naval — Breve análise do cenário brasileiro em 2007. Série de Cuadernos da Indústria. CGEE, Centro de Gestão e Estudos Estratégicos. Brasilia, 2008.

BOTTER R.- TDR 003/2018 Projeto FEMAR - Transporte Marítimo no Brasil, Escola Politécnica da Universidade de São Paulo, Departamento de Engenharia Naval e Oceânica, 2018.

CENTRO EUROPEO PARA LA COMPETITIVIDAD, Estudio de mercado para la integración productiva de cadenas de valor en las zonas económicas especiales como factor de atracción de inversiones para el sector de la industria de embarcaciones y auxiliares mexicana y diseño del Clúster Naval Mexicano (Volumen 1), Secretaría de Economía Confederación de Cámaras Industriales de los Estados Unidos Mexicanos, Jalisco, Méjico, 2016.

ECORYS Research and Consulting - Study on Competitiveness of the European Shipbuilding Industry, Sectoral Competitiveness Studies — ENTR/06/054, Rotterdam, 8 October 2009.

OETINGER, L. - Diagnóstico y Análisis de la Industria Naval en la Comuna de Valdivia, Escuela de Ingeniería Comercial, Universidad Austral de Chile, Valdivia, 2005

ORGANISATION FOR ECONOMIC COOPERATION AND DEVELOPMENT(OECD) — State owned enterprises in the shipbuilding sector, OECD Science, Technology And Industry Policy Papers No. 98, February 2021.

PODETTI, R. - Argentine Shipbuilding Industry, 100 Years (1937-2036). First Edition. Buenos Aires, 2018. Blue Industry Collection, www.industianaval.com.ar ISBN 978-987-427342-0

PODETTI, R. - Shipbuilding Industry in Brazil, 100 Years (1960-2060), 28° Congresso Internacional de Transporte Aquaviário, Construção Naval e Offshore. Rio de Janeiro Brazil, October 19-21 2020.

PODETTI R., BRAÑAS, C., and SANCHEZ CHECA F., - Dragado Inclusivo, Sustentable y Competitivo. First Edition. Buenos Aires.Vector Naval. Facultad de Ingeniería de la Universidad de Buenos Aires, 2021. Colección Industria Azul. www.industrianaval.com.ar ISBN 978-987-86-8720-9

UNITED NATIONS INDUSTRIAL DEVELOPMENT ORGANIZATION (UNIDO) - Competitive Industrial Performance Report 2012/2013, Vienna, 2013.