Analysis of the current stage of the Brazilian Maritime Industry and study of clusters features in this industry - Naval construction, repair, offshore and nautical

Rui Carlos Botter1

Delmo Alves de Moura2

Abstract

The present work aims to analyze the Brazilian maritime industry. The core of the work is making an analysis of which are the basic elements to insert this system in the national maritime industry and how it is structured nowadays. The focus of the work is to analyze the four larger segments of this industry in Brazil: shipbuilding, construction of off-shore platforms and ship repair. The research included fieldwork in each national shipyard and other actors in the supply chain of that industry, as well as unions and associations.

Key words: brazilian maritime industry, european maritime clusters, competitiveness.

Resumen

El presente trabajo tiene como objetivo el análisis de la industria marítima brasilera. El núcleo del trabajo es el hacer un análisis acerca de cuáles son los elementos básicos que se necesitan para introducir este sistema dentro de la industria marítima nacional y acerca de la forma en que está estructurado hoy en día. El enfoque del trabajo es analizar los cuatro segmentos más grandes de esta industria en Brasil: los astilleros, la construcción de plataformas marítimas, reparaciones náuticas y navales. La investigación incluyó trabajo de campo en cada astillero a nivel nacional y demás actores dentro de la cadena de suministro de dicha industria, al igual que las asociaciones y sindicatos.

Palabras claves: industria marítima brasileña, clusters marítimos europeos, competitividad.

Date received: November 3rd, 2009 - Fecha de recepción: 3 de Noviembre de 2009

Date Accepted: December 14th, 2009 - Fecha de aceptación: 14 de Diciembre de 2009

________________________

1 University of São Paulo - Oceanic and Naval Engineering – Polytechnic School, Brazil. e-mail: rcbotter@usp.br

2 Federal University of ABC – UFABC. Ph. D. at University of São Paulo - Oceanic and Naval Engineering – Polytechnic School, Brazil.

e-mail delmo.moura@ufabc.edu.br

............................................................................................................................................................

Introduction

One of the focuses of this article is to analyze if there is some indication of cluster formation in the Brazilian maritime industry when all its segments are analysed. Another focus is to check whether it is possible to be competitive in the global market. Also, the article tried to observe if Brazilian maritime segments have potential for becoming competitive and developing into a business management model for other segments.

Theoretical review of concept of clusters

One of the most important mentors who treated the subject was Marshall (1985), who dealt with the industrial concentration and the advantages these types of companies could get. He noted that the concentration of industries in one specific geographic region could lead to scale profits, consequently, transforming the economy of that region. Marshall’s studies on British industrial districts have inspired many authors to enrich literature, searching on the agglomerations of small companies located in the same geographical area.

Based on Marshall, Krugman (1995) says that the geographic concentration originates itself in the interaction between increasing returns, costs of transport and demand and it is based on the resulting agglomerations of the local externalities. Krugman’s hypothesis is that the main focus to occur geographic concentration of companies is essentially the economy of scale. This would justify the tendency of costs reduction of transport.

Clusters are formed only when the sectorial and geographical aspects are present. Therefore, cluster or agglomerations are companies of the same segment that are found installed in a nearby geographic area, with legalized and integrated relations, generating knowledge and development for all the actors of this industry (Amato Neto, 2000).

Clusters started to have a larger repercussion after Michael Porter presents its studies in 1990 which originated the base for the competitive advantages of nations. Cluster is the geographic concentration of interconnected companies and institutions in a particular area (Porter, 1998). Cluster is also characterized for involving important approaches of companies and other important institutions for the competition. In that system, all the actors of a specialized supply chain are involved, such as producers of machines and equipments, or suppliers of services and infrastructure. Clusters must consider not only the upstream or downstream, but all the support chain to the consumer, like the companies that complement the products offered to the market, the institutions and other businesses which participate with their specialties and/or abilities in technologies. Clusters also must include the Government and the universities, providing specialized training, education, information, research and technical support.

According to Porter (Porter, 1999; p. 211), a cluster or agglomerate is: ‘a grouping of geographic concentration of interrelated companies, and correlated institutions in a determined area, connected for common and complementary elements'.

Porter based on his Diamond Model for the competitive advantage of nations. In this model, the dynamic interaction between demand conditions, strategy, structure and rivalry of the companies are analyzed on a systemic way (Porter, 1991).

According to Suzigan (2006), Porter accomplished his studies in the analysis of the regional agglomerations, contributing in the area of business economics to the financial health of the companies. That way, he has approached that the competitiveness of the companies in clusters are based on four sets of favourable conditions that predominate in the local environment of business: production factors; demand; presence of suppliers and service industries; and rivalry and strategies of competition from the local companies. Suzigan, et al. (2006) make a vast review on the literature referring to the definition of clusters, agglomerations and local systems of production and describe their peculiarities and the variables inherent to each model.

Garcia (2006) analyzes the vision of Marshall, Krugman and Porter about the benefits of the agglomeration of the companies, focusing only the local externalities that emerge spontaneously from the concentration of the producers. The conclusion of the work stands out the importance of these externalities to the local producers that can access a set of knowledge, abilities and services, reduction of costs and increment of the competitive capacity. The elements that corroborate the externalities are: the presence of qualified labour, raw material suppliers, components and equipments suppliers and the occurrence of spill-over of technologies, abilities and knowledge.

Thus, a cluster aims at an increase of reliability, dissemination of know-how, technological qualification of the actors and innovation in the productive processes of the products and services offered. The result is the increase in value of the industries and institutions of the sector.

Gordon & Mccann, (2006) approached that the second model of space cluster which emerged of the traditional economy or neoclassical economy is the industrial complex. The first model was agglomeration. They told that the industrial complex is characterized by the term of business relation among the companies, in what refers to the purchases and sales of products or service. Another aspect analyzed by Gordon & Mccann is the reduction in costs of transport, because of the proximity among the companies. The reduction in costs of communication is other important factor in the proximity among the companies in an industrial complex.

In the ideal cluster, the economy of scale is reached by the total cooperation among the actors of the agglomeration, bringing mutual benefits to all the productive chain. The objective of a cluster is to be able to, physically, have companies close one to the others, promoting contribution. However, it is not always possible (Dijk; Sverrisson, 2003).

Physical proximity is only one of several items which characterize a cluster. The other features are: technological cooperation among the companies, long term contracts, shared ethics in businesses, presence of a reasonable number of companies with similar or subsidiary activities. Items related to the characteristics called ‘constructed’, also corroborate the formation of cluster, as a mutual process of collective learning, relationship created by the transactions among producers and traders, the function of the region in the institutions nearby, such as schools, universities, research and development centres, the function of the municipal, state and federal agents, the level of technology of the region, labour, etc.

There are three forms related to the formation of a cluster and they are characterized as follow. The first one mentions the pure agglomeration, proceeding from the economy of scale and target that flows from the companies located in the same geographic area. This brings three main benefits: the companies can get more prepared labour, can access a larger range of products and services with superior quality and they can get profits related with the information flow and ideas generated inside the complex. The second form of cluster refers to the industrial complex. In this case, the companies are situated next to each other for minimizing the costs of communication, transport and logistic system. The third form of cluster is the social chain where the companies relate themselves, searching for cooperation, aiming to promote loyalty and mutual interest in the businesses, long-term contracts and interpersonal relationship (Turok, 2003, Simmie; Sennett, 1991).

There is a variety of definitions in literature, but there is the tendency of using terms such as agglomeration, industrial district etc. Sennet, Simmie (1991) make a vast review in literature on different types of implemented clusters in several countries, and describe variables necessary to characterize clusters related to the innovation, therefore these variables can be the competitive differential for the companies faced their competitors and can signify profitability and survival along the time (Sennett, 2001, Simmie; Sennett, 1991).

Not all grouping of companies from the same branch can be considered a cluster, and, sometimes, it can only be considered as an industrial district (Meyer-Stamer; Altenburg, 1999).

Schmitz (2000) analyzes four clusters: in Guadalajara, Mexico; in Vale dos Sinos, Brazil; in Sialkot, Pakistan; and in Agra, India. Schmitz studies the behaviour of the variable cooperation in these clusters and verifies whether this variable collaborates for the competitiveness of the searched clusters. In some clusters, the variable is a competitive differential for the success, while in other ones it has average relevance for the businesses.

When a cluster is analyzed, it is essential to evidence the presence of local externalities related to the size of the market, specialized labour and technological spill-over (overflow) which could favour the local specialization, besides linkages of production, commerce and distribution. There must be cooperation in marketing, promotion of the exportations, supplying of essential inputs and also research and development, in order to reach balance between competition and the cooperation. All the companies of a cluster must benefit themselves with the support from the local institutions. There are private and public actions that can corroborate the development and the promotion of a cluster. The engagement of adjusted policies, social and cultural identity can all promote confidence and exchange of information among the companies, benefiting the set of organizations (Suzigan, et al. (2006).

The external economies can be called of services or profits that a producer provides to another one without any compensation (Igliori, 2001). The external economies can, thus, be classified in three great groups: technological economies, market economies and economies of organization. The technological economies involve impacts in the function production and become directly related with technological standards (innovation in the market and in the production process) adopted: physical conditions - climate and ground, etc. - offer of raw materials, infrastructure of transport, etc. (Machado, 2003).

Implementation of clusters

Waits (2000) approaches the composition of the essential agents from the aerial-space segment and the formation of the three main levels, such as leader companies in the exportation, support companies and the specialized foundations that compose the plan of economic and strategic development from Arizona. In the State of Arizona, a programme called ASPED was implemented, that means, Strategic Plan for the Economic Development of Arizona, and nine groups of clusters have been implemented.

Each cluster had an economically representative leader company for the sector in study. Arizona’s Government has chosen a representative for each cluster that is responsible in selecting actors that represent several levels of each cluster formed of small, medium and large companies related with the final production, as well with the supply chain.

Each cluster also had a representative from Universities, from chambers of commerce, lawyers and marketing companies. The member was responsible for pointing out the necessities and inherent opportunities of each segment to the groups. Each cluster had five great demands to be executed:

• Cataloguing the main components of each segment as well as mapping the inter-relationship among the companies;

• Articulating a vision that could be reached over what each cluster could become in the next 10, 20 years;

• Identifying chances of growth of each cluster in a direction desired for the expansion of the companies and preferably attracting new ones from other regions;

• Identifying chances of larger synergy inside of each cluster; and

• Identifying necessities of specific economic justification and proposed strategies.

According to Waits (2000), the concept of industrial clusters has been contributing immensely to the policies of the State of Arizona, with the educators and the economic development of the region, fortifying the enterprises and adding value to the clients. After the implementation of the ASPED, the authorities that elaborate the policies in the State of Arizona started to understand the importance of being competitive, developing economic strategies for the 21st Century, focused on the industries guided for the global market. Consequently, with the new strategies of industrial policies for the State of Arizona, some specific objectives hve been also lined up, as more qualified works and high standard of living to the citizens of the State.

Altenburg; Meyer-Stamer, (1999) tell the experience of clusters in Latin America and emphasize that these agglomerations are characterized by small and micro companies with low entrance barrier, little specialization of labour and products with low technology. Altenburg; Meyer-Stamer also success cases as the one from Chile, called Proyectos de Fomento (PROFOs), which is a three-year contract among a group of five or more from small companies and agencies of public or private support, considered as a network broker. These groups receive assistance for integrating its activities, such as market research, studies of economic viability, or to participate commercial missions or fairs.

There is the experience from Denmark in the implementation of the first studies about cluster (Drejer, et al., 1999). They approach several clusters that were analyzed and implemented, as well as state that among the ten countries used for Porter in its research on competitive advantage; clusters implemented in Denmark has served as study base.

Floysand; Jakobsen (2001-2002) analyzed the internal factors related with cluster of fishery in Norway, and told the potential problems inherent to the system focused on the social ambit. The research mentions the degree of rivalry between the competitors of cluster and the way they duel for inserting and keeping their products in the international market. The article shows another side of the cluster, different from several authors regarding to the cooperation among the companies, exchange of information and team work.

Worldwide maritime clusters

All clusters must have, at least, one company that is considered a leader, for being able of multiplying the knowledge for the other ones of the chain. The leader company should have the following characteristics: to be engaged with Research and Development and to have access to the international market (Langen, 2002).

The Norwegian maritime cluster is composed of Norwegian associations of navigation, Norwegian federacy of engineering and industries, associations of metallurgic workers and maritime associations, of companies that own boats, shipyards, industry of maritime equipments, brokers, financial companies, insurance companies, consultancies, etc., totalizing over 600 members, including governmental representatives. They have these goals: defining the industrial policies; promoting the cooperation among the members of different sectors inside of the maritime chain; and promoting the international businesses, benefiting the Norwegian maritime industry.

The Norwegian maritime sector employs around 75 000 people in the following maritime sectors: naval construction; repairs; industrial equipment; industry of oil and offshore; the association of the companies of maritime navigation; coastal shipping companies; ports; consultancies; institutions and research centres; training and education institutions; brokers; financial companies and banks; insuring and engineering (Langen, 2002).

In Norway, the maritime cluster begun around the year of 1990 and was opened for all the companies and organizations that, somehow, were related to the maritime industry. It was necessary the commitment for the employers to the employees, so that the idea of cluster was implemented successfully. Organizations such as the association of companies of the Norwegian navigation, federacy of the Norwegian industries of engineering, association of workers of metallurgic industry and Norwegian association of workers of the maritime sector, shipyards and repair, industry of oil and offshore, research institutes, maritime equipment companies, brokers, financial companies, insurance companies, and consultancies, eight regional organizations, ports, education centres, training institutes and governmental agencies, were some of the 600 members that participated in an integrated way for the discussion of the problems and implementation of the maritime cluster concept for benefiting the local maritime industry (Lahnstein, 2004).

The initial objectives defined for implementation of the Norwegian maritime cluster were: defining industrial policies, promoting cooperation among the companies of the segments related to the maritime industry and inserting the Norwegian products in the international market.

The maritime cluster was implemented in the country in 1996, after six years of discussion with all of the actors involved with the Norwegian maritime industry. But it was only in 1996, that the industrial policies were, in fact, used by Norway. For a cluster to be a case of success, it is basic to follow some steps, such as: defining cluster, establishing its importance, promoting visibility in the domestic scene, defining industrial policies, establishing the demand of the sector and promoting commitment of the supply chain, monitoring and keeping the defined levels and the strategies, promoting exportation and internationalization, promoting innovation, research and development, mainly for the leader companies, and establishing goals for reaching the necessary education for the labours, supplying the market (Lahnstein, 2004).

The case of Panamanians maritime clusters started at the construction of The Panama Canal that has assisted in the competitive necessity of the horizontal and vertical maritime industry. The service segment is directly related with the Panamanian maritime industry that is the great stimulus to the economy in the country. Panama’s GDP in 2001 was of 10.25 billion of dollars. This year, the businesses related with the maritime industry have represented 1,971 billion of dollars, approximately, 19.22% of the GDP, and have employed 26,875 employees connected to the sector (Maucci; Lugo, 2002)..

There are five large central activities which support the economy: The Panama Canal, Ports, Register of Vessels, Free Zone of Colon and Fishery. About the related industry and the other maritime services, it can be cited: Maritime industry; Pilotage; Fuel supplying; Maritime research; Dredging; Companies of navigation; Logistic operators; Services of repairs; Centre of maritime training; Travel agents); Other Sectors; Hotels; Restaurants; Centres of specialized training; Airports; Banks; Financial companies; Tourism; Insurances; Activities of recreation and Commerce, in general (Maucci; Lugo, 2002).

In The Panama Canal, approximately, 4 000 ships per year generate 14 000 tickets, which generate activities related with supply of fuel, repairs of boats, ports specialized in the movement of containers and liners (Maucci; Lugo, 2002).

The flag registration of vessels also involves an enormous contingent of companies and people directly involved with the maritime service. The Free Zone of Colon is a worldwide logistic centre, generating thousands of jobs and stimulating the economy of the Country. The industry of fishery also generates thousands of direct and indirect jobs.

The Belgian maritime cluster is characterized by a small number of companies that are considered of great deadweight, and these ones occupy prominent position inside of certain specific segments of the market, or are companies of large international repercussion, as in the case of the sector of hydraulic engineering. Belgium has perceived that it was necessary to have companies of prominence inside specific niches that have corroborated, excessively, the implementation of maritime clusters in the country.

The Danish specific sectors that form the maritime cluster are: the waterway transport, maritime services, naval construction, maritime equipment, offshore for gas and oil extraction. The companies are supported by institutions related with the governmental authorities of the country, universities and centres of technological research, technical schools, centres of training and associations of class, companies related with the productive chain of each maritime segment and financial or insurance companies. There is integration among the actors that participate of the Danish maritime cluster with focus in promoting the national development, and the country can be competitive in the world-wide maritime activity, inside some specific niches (Drejer, et al., 1999).

In the year of 2004, Denmark had: 17 companies of navigation; one shipyard; 12 companies of ship; three companies related with the port authority; 13 education and research centres; four institutions related with the governmental authority; ten companies of maritime commerce; 27 consultancies and service; and, five companies related with the financial sector and insurance (Drejer, et al., 1999).

In the year of 1999, 37 out of 1 000 people acting in the work market were related with the activity of inland trade, 78 were related with the segment of maritime services, 24 with the segment of naval construction, 54 with the segment of maritime equipment, three with offshore, representing approximately 7.2% from the total of the Danish economy. Therefore, the Danish maritime cluster is highly meaningful for that country when compared to its economy (Drejer, et al., 1999).

After the year of 2004, the cited numbers above grew more, stimulating the Danish economy, since there has been a bigger integration among the pertinent actors of the maritime sector. An association was created to approach the actors, to organize the segments and to discuss the common particularities that they had the common interest. Several conferences and meetings were necessary to promote the synergy among the integrated actors. A strong campaign of international marketing was carried out to promote the image of the country related with the maritime segments. The association which was created had also the objective to promote and stimulate the research, to develop products and services with technological value, specially, with the education of superior and technical schools. It was necessary to have partnerships with many related European associations with the maritime area and with excellence centres in research for development of qualified and specialized labour (Drejer, et al., 1999).

The Dutch maritime cluster was one of the pioneers in Europe, initiating its activities in 1996; and, in 1997, it was established an association called Dutch Maritime Network for managing this activity and to give the total support to its implementation in Holland. The Dutch maritime cluster started its implementation with the following maritime segments: sector of navigation, naval construction, ports, inland trade, dredging, offshore activities, equipments suppliers, Dutch navy, maritime services, nautical and fishery industry.

An intense work in all Dutch community for implementation of cluster was carried through, with the participation of the society, the government and the actors of the maritime segments. This spreading has involved means of communication such as journals, specialized publications in the maritime segments, television programmes, advertisements in schools, visits to the ports, electronic media and websites. That was the initial form to promote this type of discussion for all the society and to integrate all the Dutch maritime actors for the growth of the Dutch maritime industry (Nijdam; Langen, 2003).

The competitiveness of a cluster depends on the interaction among the companies related with it. From the total of € 70 billion of aggregated value produced by the European maritime industry in the year of 2001, 10% of this value was generated by cluster of the Dutch maritime industry. To structure a cluster, it is necessary to have a leader company in the market that attracts the other companies related with the segment. In Holland, the implementation of maritime cluster has always had as starting point, the adhesion of a leader company (Nijdam; Langen, 2003).

A leader company is likely to be the one that possess a definite impact in the other ones related to the cluster in analysis. It must be capable to contribute with the competitiveness of its partners, sharing knowledge, adding many companies of the sector, contributing to add value in all supply chain of the sector. It also must occupy a central position due to its relationship with the supply chain and final customers. The one must surpass for the changeable innovation, as much in the process as in the products.

The leader company should have an outstanding position in the market, stimulates the development of new abilities and knowledge for the sector, and stimulates new investments permeating this knowledge to the other companies related to the sector, making, thus, the natural growth of cluster in which is placed. The benefits of the externality transmitted to all the companies related to a determined cluster is a principle that characterizes a cluster, therefore when only some companies of any segment are benefited due to this externality (acquired knowledge), this do not characterize a cluster, but an industrial district or something similar to that (Nijdam; Langen, 2003).

Investment in externality of the leader company includes investments in innovation and internationalization. The knowledge must be permeated to all the companies of the cluster. Other essential factors for a cluster to obtain success are: investment in training and education, knowledge and information related to the necessary infrastructure aspects to all the companies related with cluster. This set of factors assists, excessively, the competitiveness of the cluster (Nijdam; Langen, 2003).

To determine the leader companies in each Dutch maritime segment, in order to carry through the conception of cluster, the following methods were used: interviews with the associations of class from each maritime segment to get information about the leader companies in the vision of the associations because they needed to be based on some criteria. They are: first, the size of the company analyzed by its turnover, the number of employees and its invoicing; second, the number of subsidiaries outside the country, because it measures the internationalization of the company; third, number of patents, because it measures the ability that the company has for innovation; and fourth, number of companies inside of an association in which one organization is admitted, because that fact is linked with the negotiation power with the governmental agencies ((Nijdam; Langen, 2003).

The actors related with the maritime industry were heard for the implementation of the Finnish cluster. Moreover, it had the intense support of the Ministry of the Communication of that country and the Ministry of the Finances, Commerce and Industry as well as the Centre of Finnish Maritime Studies. The preliminary studies for implementation of cluster in Finland initiate in the year of 1991, after the country had been invited to participate on a research developed by Michael E. Porter in 1987 and 1988, referring to a study on competitiveness in ten countries (Viitanen, 2003).

Viitanen (2003) says that the cooperation among the companies in a cluster is very important, therefore, the innovation and the development can be permeated through all the companies, benefiting the set and not one or another company. This would be a way to assure the competitiveness among the companies and with this, the possible threats related with cluster would be better managed and eliminated or minimized.

The structure of a cluster must contain, at least, one company that is considered leader or a set of companies that produce products considered essential. There must be support companies considered suppliers of the leader companies and, also, associations of class, universities, educational centres, research centres, financial institutions and government [26].

Finn maritime cluster has developed itself around of two main segments: naval construction and construction for transport of passengers. During the Second World War, the Finnish shipyards were requested to supply the fleet of the old Soviet Union and, also after the Second World War. They have also specialized in naval repair segment (Viitanen, 2003).

In the end of 1985, big groups of naval construction were in difficulties, and it was necessary to structure this industry. With the economic contraction of that period and the end of the order of naval construction from the extinct Soviet Union, the scenery of the Finnish naval industry was summarized in a shipyard focused in the products of offshore construction, a specialist in the construction and development of projects focused in the area of vessels construction in the transport of passengers, luxury cruises, ferryboats, vessels boats for patrol and defence and ice breaker ships, and another one in the naval construction, such as, for example, LNG ships. In the segment of passenger liners, Finland is ones of the first in the world, when it refers to the exportation of products.

These are the main products that are produced in the Finnish maritime industry: cruise ships, ferryboat for the transport of automobiles, cargo ships, ice breakers, special patrol ships, special ships for research, special tanks and offshore. Factors that has contributed to the maritime industry of this country are: know-how of engineering,

know-how of the technology required, know-how of development and projects, quality systems, the environmental and the security technology (Viitanen, 2003).

Several other segments contributed to structure the Finn maritime cluster, such as: steel industry, metal mechanics industry, industry of pieces for ships, industry of interior projects in vessels, electronic industry, hydraulically engineering, among others. Services were also part of this process, such as: financing sector, insurance sector, research centres, workers associations, and repair and maintenance services.

European maritime clusters

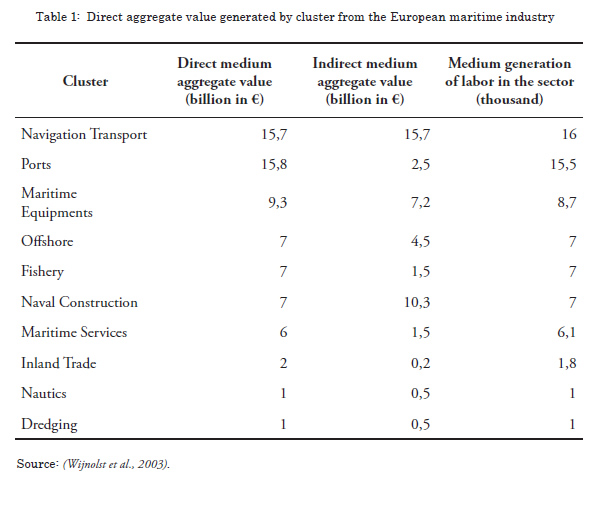

The aggregate value of cluster from the European maritime industry (European Community) in the year of 1997 was approximately € 159 billion. The direct value generated by the industry of cluster from the European maritime industry was of, approximately, € 70 billion, as shown in table 1 (Wijnolst et al., 2003).

Navigation/Transport: the financial movement was of, approximately, € 48 billion in 1997. The navigation/transport is the biggest maritime sector in Europe, and Norway was the country that was more benefited from this type of financial movement, followed by Denmark, Germany, the United kingdom, France, Italy, Sweden, Holland, Greece, Finland, Belgium and with really small parcels in this analysis sector, there are Portugal, Ireland and Spain.

In accordance with the European Commission, the cluster in study (Navigation/Transport) has obtained € 15,7 billion in financial profits, and the most benefited countries, ordered by monetary value in €, were: Germany, the United Kingdom, Norway, Denmark, Italy, France, Greece, Holland, Sweden, Finland, Belgium, and with really small parcels, we have Portugal, Spain and Ireland (Wijnolst et al., 2003).

• Naval construction: the financial movement in 1997 was of, approximately, € 10,3 billion in new constructions, € 5,7 billion in repairs and conversions, and € 3,4 billion in the naval construction. The leader countries were: Germany, Italy, Norway, Finland, Holland, Denmark, France, the United Kingdom, Spain, Portugal and Sweden.

• Maritime equipments: the financial movement, in 1997, was of, approximately, € 22,4 billion. The countries that were more benefited were: Germany, the United Kingdom, Norway, Italy, France, Holland, Spain, Denmark, Finland, Sweden and Greece.

• Port and Ports Services: the financial movement was of, approximately, € 15,2 billion in 1997. The most benefited countries benefited were: Belgium, Italy, Holland, Spain, Germany, the United Kingdom, France, Denmark, Sweden, Finland, Portugal, Greece, Ireland and Norway.

• Offshore: the financial movement was of, approximately, € 16,4 billion in 1997, concentrated, practically, in four countries: The United kingdom, France, Norway and Holland.

• Inland trade: the financial movement was of, approximately, € 3 billion in 1997. Two countries dominated the sector: Holland and Germany, due to its localization next to the River Reno basin.

• Fishery and Aquiculture: the financial movement was of, approximately, € 11.7 billion in 1997. It is one of the biggest sectors in Europe. Four countries have the biggest sectors of fishery and aquiculture: Italy, Spain, Norway and France.

• Dredging: the financial movement was of, approximately, € 2,9 billion in 1997, practically concentrated in two countries: Holland and Belgium.

• Maritime services: the financial movement was of, approximately, € 10 billion in 1997. The United Kingdom possesses the biggest parcel, followed by Denmark, France, Germany, Italy, Holland and Norway.

• Yachting: the financial movement was of, approximately, € 3 billion in 1997. Three countries dominated: France, the United Kingdom and Italy.

The direct value generated by the European maritime industry was estimated in € 70 billion and constituted almost 1% of the European gross domestic product in 1997. The aggregate value corresponded to 44% of the invoicing in the maritime sectors (total of € 159 billion). The total labour, estimated, was of 1 545 000 people. Around 33% (about € 23 billion, out of the € 70 billion), generated by the direct aggregate value returned to the governments in the form of taxes and social contributions. The sum generated by the direct aggregate value of the maritime industry was used in investments in the private sector. The private sector has consumed € 16 billion, from the € 70 billion, and the investments were of € 19 billion. But only 17%, of the € 70 billion - (€ 12 billion) were expended in services and goods outside of the European Union (Wijnolst et al., 2003).

Europe, in order to become world-widely competitive and to face the Asians, such as Japan, South Korea, China, Singapore etc., has adopted the strategy to compete in the segment of ship construction with sophisticated ships, in special, the ones of passengers, besides the emphasis in the industry of ship pieces, with products of high technological value. In 2004, the total production of Europe, in terms of delivery in CGT, was inferior to the production in South Korea, nearly three times smaller; however, in terms of revenue, the European shipyards obtained almost 10% more (€ 1 billion) than the ones from South Korea (Coutinho, 2006).

Methodology

For the research, 31 shipyards were visited in Brazil. From this total, 14 shipyards are from the segment of nautical construction, tourism and leisure. There are 20 shipyards which belong to an association of class from the nautical segment. The most representative shipyards, in terms of sales, for domestic and international market, and in terms of volume of production were visited personally for data collection (research in field).

In the segment of ship construction, there are, currently, nine shipyards in Brazil and seven were visited for application of the questionnaire. In the platform segment, there are five shipyard/ EPC (Engineering, Procurement and Construction Contracts) and all had been visited. In the segment of ship repair, all the five shipyards were visited personally.

The methodology consisted in the qualitative type research (Mattar, 1999; Cooper; Schindler, 2003; Babbie, 2001; Selltiz Et. Al., 1987; Botelho; Zouain, 2006). It was carried through by means of personal interviews, with entrepreneurs, presidents, directors and managers of the maritime industry. The criterion used for election of the companies in the qualitative research was based on the importance of the company inside its segment. Therefore, the questionnaire was applied exclusively in the 31 visited shipyards. However, other data had been collected personally in the other actors of the national maritime industry.

Current scenery of the Brazilian maritime industry

In the State of Rio de Janeiro there is a concentration of shipyards focused on the segments of the ship construction, repair and offshore platform construction. Analyzing the geographic localization aspect, these segments of the Brazilian maritime industry have a strong characteristic of cluster (Porter, 1999). However, the geographic aspect is not enough to evidence the cluster. When it is analyzed the integration factor among the shipyards of these segments in the State of Rio de Janeiro, the research has pointed out that is almost inexistent the exchange of experience, know-how, technology or knowledge among the companies. Few are the suppliers that participate on the development phase of products from the shipyards and when this occurs, it is generally in the offshore platform segment where there is the PROMINP programme and the leadership of Petrobras, that contributes for the small integration among the companies of this specific segment (offshore platform construction). The integration with the other actors of these segments, such as universities, research and development centres, government, etc. is isolated and without industrial policies that contribute for the development of the Brazilian maritime segments. Most of the supply chain of these segments is geographically distant from the state of Rio de Janeiro.

When the segment is analyzed, it is evident that there is not a cluster; therefore the shipyards are installed in several places in the country, with enormous distances among them and also with their supply chains. There is not any kind of integration among them, not even integration with universities, research and development centres, government, and the other actors from the nautical segment. There isn’t currently any industrial policy which contributes for the development of this segment in Brazil and of its supply chain, despite being a promising segment to the insertion of products in the North American and European market (Moura, 2008; Moura; Botter, 2009).

There is in Brazil a programme called PROMINP - programme of Mobilization of the National Industry of Oil and Natural Gas, coordinated by the Ministry of Mining and Energy, with the objective of maximizing the participation of the Brazilian industry of goods and services, in competitive and sustainable bases, in the implementation of projects of oil and natural gas in Brazil, and also abroad.

PROMINP project is focused on implementation in the areas of exploration and production, maritime transport, supplying, gas and energy and ductway transport. The focus is to identify and to implement qualification actions of the industry, on a way to take care of the demands of the projects in investment from the operators of the oil and natural gas sectors. It has the participation of the Ministry of Mining and Energy (MME), of the Ministry of Development, Industry and Foreign Trade (MDIC), of Petrobras, of The Brazilian Development Bank, of the National Organization of Oil Industry (ONIP) and the Brazilian Institute of Oil and Gas (IBP), that congregates all the Brazilian operators. The National Confederation of Industry (CNI) and the following class associations also participate: Brazilian Association of Industrial Engineering (ABEMI), Brazilian Association of Engineering Consultants (ABCE), Brazilian Association of the Infrastructure and Base Industries (ABDID), Brazilian Machinery Builders' Association (ABIMAQ), Brazilian Association of the Electric and Electronic Industry (ABINEE), Brazilian Association of the Industry of Pipes and Metal Accessories (ABITAM) and National Union of the Industry of Construction and Naval Repair and Offshore (SINAVAL).

PROMINP developed its first studies in the years of 2003/2004. In that period, it was evidenced the necessity of qualification of an enormous number of labour. The results identified by the diagnosis system, pointed to the necessity of a demand for qualified labour, until the end of 2007. Thus, a huge effort became urgent aiming at specialization and professional education.

After many months of study, it was conceived, then, the Plan of Professional Qualification of PROMINP, which has the objective to structure actions for qualification of labour in the 150 job categories considered critical in the diagnosis.

In order to take care of the total demand of 70 thousand qualified professionals until the end of the year of 2007, 64 thousand professionals of basic and technician levels, and 6 thousand of graduate education will be trained, involving more than 40 education institutions. 580 courses and 3 800 groups in several Brazilian states, It is foreseen an investment around US$ 110 million (Moura, 2008; Moura; Botter, 2009).

PROMINP project in Brazil is much similar to the cluster system of the maritime industry implemented in Holland and Norway and, it is a model that can be expanded to the other segments of the Brazilian maritime industry; therefore, it involves many agents who are direct or indirectly related with the national maritime industry.

As this programme involves an expressive number of organizations, and there is enormous demand for products with assured quality by Petrobras (the final customer), it is observed the existence of a bigger demand for qualification of the suppliers of parts and equipments.

It is important to stand out that in the segment of platform/UEP/FPSO construction, it is a requirement of Petrobras that the supplier possesses products/components/parts with assured quality and this factor collaborates so that 100% of construction companies (EPC), or shipyards have qualification. That way, two negative points inherent in the domestic maritime industry could be eliminated with the implementation of models similar to PROMINP and to the other segments of the maritime industry: qualification of the suppliers and qualified labour.

Being competitive in the maritime industry demands the necessity of qualified labour, and, currently, only the segment of platform/UEP carries through some type of investment with this purpose. The shipyards train this specialized labour directly in its physical installations to supply, exclusively, their necessities. A school such as Senai (National Service for Industry), is a great generator of labour for the sector, the Armory of Rio de Janeiro’s Navy also possesses professionalizing courses that prepare specialized labour for the sector. Inside of the PROMINP programme, the qualification of the labour, for the sector of platform/UEP construction is foreseen, due to the necessity of constructing platforms for Petrobras.

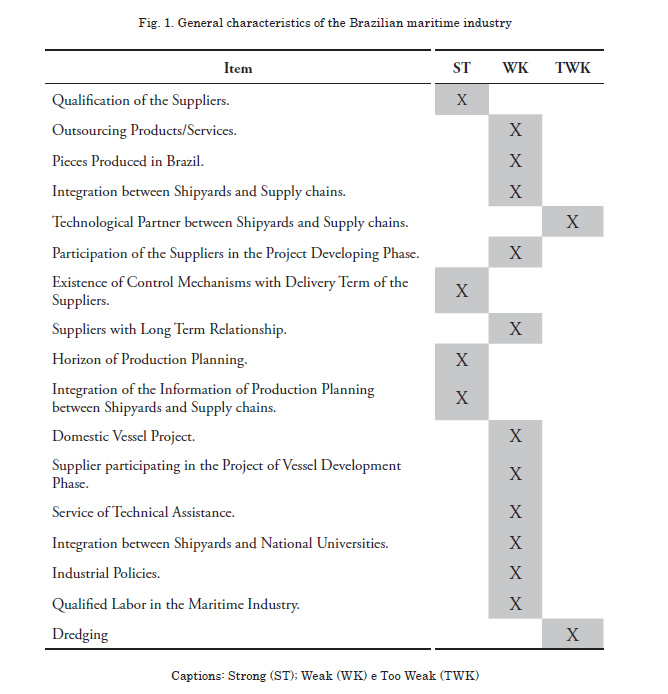

Fig. 1 demonstrates on a punctual form, the strong, weak and very weak points of the Brazilian maritime industry. For Brazil to become world-wide competitive in this industry, it is necessary to have a national plan of development that involves all or the main direct and indirect actors from all the segments. It will be necessary to have an involvement and commitment of governmental spheres, unions, associations, owners, universities, research and development centres, technical schools, industry federations, confederation of industries, services, agencies of research and technology (Moura, 2008; Moura y Botter, 2009).

Fig. 2 presents the division for segments of the Brazilian maritime industry and describes the characteristic of these sectors in relation to the following points: whether the segment is on a strong, medium or weak phase in relation to the critical points for being competitive in the sector. The conclusions refers to the descriptive analyses from the statistical inferences proceeding of the research in field carried through in the Brazilian shipyards (Moura, 2008; Moura; Botter, 2009).

Some important points that can be inferred originated from the analysis carried through in figure 2 and of the descriptive statistics, are:

• Competitiveness of the Brazilian products could increase with larger participation of the suppliers in the project development phase of the shipyards/EPC. The integration could result in benefits to eliminate or to reduce problems related to the production phase of the shipyards/EPC and to increase the degree of partnership among the parts. Suppliers would better understand the businesses of shipyards/EPC and could produce products focused on the necessity of the maritime industry. Also, the integration of the parts could develop suppliers to fill up international markets.

• When the participation of the suppliers in the project development phase by segment is analyzed, it is noticed that in the platform/UEP/FPSO segment, there is more integration among companies that acts in the EPCs system (Engineering, Procurement and Construction Contracts - Contracts related with a specialized company in the engineering of the project management, in the purchase of parts and components management and in the construction of the enterprise management). Some companies that act in the construction sector of Platforms/UEP are not shipyards, but, they are managers of EPCs enterprises [34].

• As there are few companies that produce, exclusively, for the Brazilian maritime industry segment, and, even though for international maritime segment, there is a small integration between suppliers and shipyards. Another relevant factor is the fact that, the demand related to the maritime industry, being small, many times, does not justify to the supplier to invest time for a bigger integration with the shipyards. The percentage of suppliers that participates as technological partner in the Research and Development area with the shipyards or companies of enterprises/EPCs management is more representative in the Platform/UEP/FPSO construction segment than in the other segments, because of PROMINP programme and, certainly, the power of the biggest customer of these types of products, Petrobras. Even in the maritime segment of platforms/UEP/FPSO construction, still, there is a field for wider integration among companies, universities, research centres to improve the participation of the companies in the products development phase, according to the opinion of the proper interviewed companies. This percentage is relatively low for the yachting segment, naval construction and Naval Repair with values of 30.8%; 33.3% and 25.0% respectively.

• The technological partnership in the Research and Development area in the Naval Repair segment is mentioned in the research because there is a shipyard which has recently signed a partnership with a South Korean shipyard and some results related with the Research and Development area has already affected positively its activities in Brazil.

By its own characteristic, the Platforms/UEP/FPSO construction segment, is much well evident, because it is clearly noticed the integration with universities, research centres, technical schools, Government, society, associations, etc. In the Naval construction segment, there is partnership when it deals with suppliers with great bargaining power in the supply chain or when it is considered strategic suppliers for the shipyards, such as supplying of maritime engines and other vital components for the shipyards business (MOURA, 2008).

There are Brazilian companies searching for bigger integration with the shipyards in Brazil, to understand, with more details, which is the real necessity of the market in terms of demand and specific products. In the Nautical construction segment, this fact also happens with the suppliers considered strategic for the shipyards and, in its majority they are suppliers of imported components.

Conclusion

As for the item cluster, the experience of implementation in some European countries can be used. It is necessary to raise all the related actors aware of having companies leading this project for integration of all the actors from the domestic maritime industry. There is the necessity of participation of the government, universities, research and development centres, employers associations, unions, workers, governmental or private financial companies, the companies of maritime and waterway transports, associations of machines and equipment producers, suppliers of essential raw material, the society, etc.

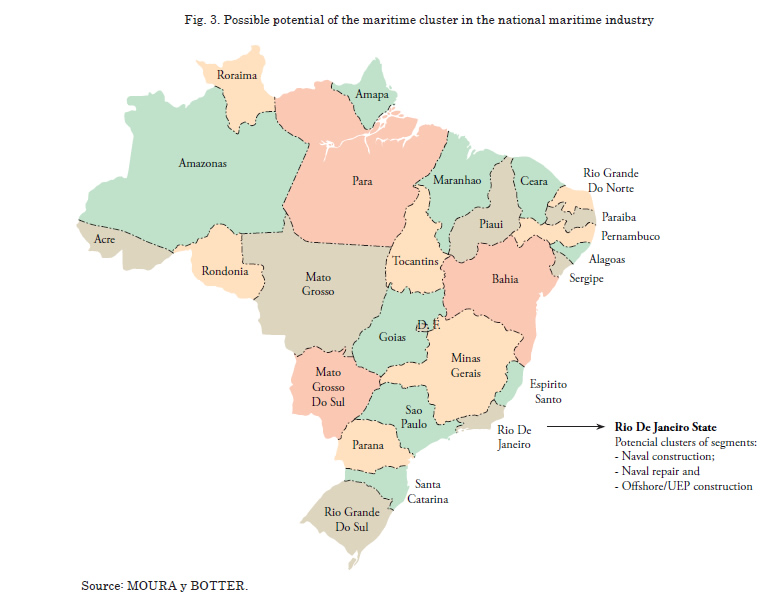

Through the bibliographic review carried through in this work, in the topic about cluster and maritime cluster, it can be concluded that the segments of ship construction, naval repair and Offshore/UEP, as in Fig. 3, installed in the State of Rio de Janeiro, have potential for cluster development, compared to the shipyards installed in other States of the country. For having a bigger concentration of shipyards in one specific region of Rio de Janeiro, as it is in the case of Niteroi, this factor contributes to the cluster development (Moura, 2008; Moura y Botter, 2009).

With the exception of the PROMINP programme, there is nothing structured among the actors of Brazilian maritime industry that characterize a cluster in Brazil but the proximity of localization among the shipyards. There are employers’ associations searching for approximating to actors related with the maritime industry, but yet, slowly. There is the necessity of having larger participation of the society, government, suppliers of machines and equipment, parts and components, universities, technical schools, research centres, etc.

PROMINP programme is much similar to the model of cluster implemented in Norway and Holland which has been succeeding. However, an enormous differential is that in the two European countries, the cluster model implemented has corroborated the increase of the competitiveness of the companies and their insertion in the globalized market, disputing considerable market share world-widely, mainly with products and services of high aggregate value and, in Brazil, the PROMINP model does not possess this characteristic and purpose.

Brazil needs to discuss with the society the successful models implemented in Europe, not imitating them, but taking advantage of the great profits and adjusting the domestic reality providing growth for the Brazilian maritime industry inside the Brazilian market, as well as inserting products and services in the international market.

In the construction of a platform, where PROMINP programme is implemented there are still products of high aggregate value or with high technology being imported, and it can be thought about the local development of some of these products, with bigger integration among shipyards, EPC, universities, research and development centres, promotion agencies, association with international universities and, mainly, qualified and specialized labour (Moura, 2008).

In the bibliographical review, it becomes evident that the European maritime clusters has always searched to the integration among the companies related with the maritime industry of its respective countries along to universities and research centres for generating specialized labour, for supplying the needs of the sectors and, moreover, for sensibilizing the society in the necessity of investments in the labour with ability and enabled to the new challenges, aiming at facing the huge competition world-wide. The proximity of research and development centres, universities and technical schools is one of the bases to initiate an implementation process of maritime clusters, such as the successful experiences in Europe.

Therefore, having leader companies that mobilize the other actors of the maritime industry of a country to work as a team in favour of all the industry, having support and integration among universities, research and development centres and technical schools and government (collaborating with public and industrial policies that promote the development of all the industry) are essential conditions to increase the businesses of shipyards, the whole supply chain, the companies of support and service and the government, because, they reflect directly on better economic and social conditions for the people, and provide foreign currency for the country, as pointed in the bibliographical review, in the cases of the European countries experiences.

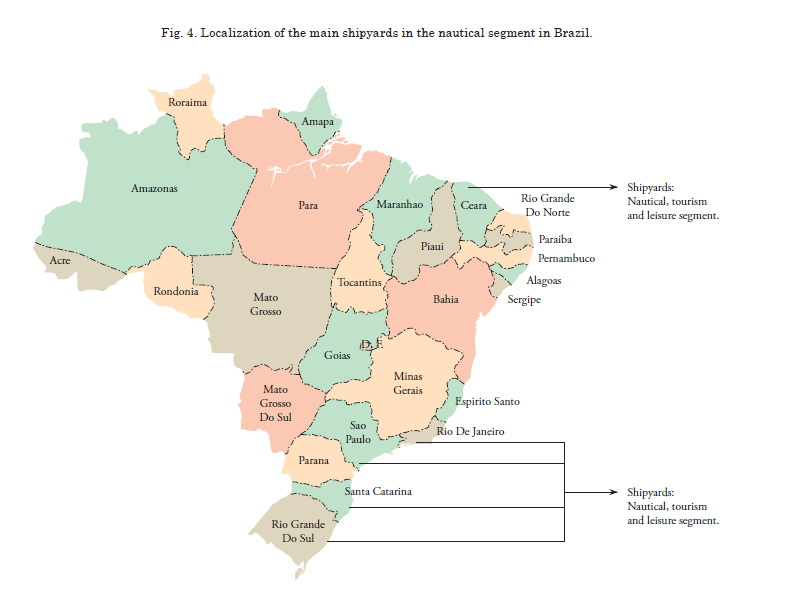

In the segment of nautical construction, tourism and leisure, there isn’t any indication of formation of cluster in Brazil. The companies are generally separated physically; there isn’t a concentration on a specific area, as showed in Fig. 4. There are shipyards spread among the States of Rio de Janeiro, São Paulo, Santa Catarina, Rio Grande do Sul and Ceará. The biggest production is found in the South-eastern and South regions, specifically, in the States of Rio de Janeiro, São Paulo and Santa Catarina. In the construction of luxury yachts, the biggest production is in the States of São Paulo and Santa Catarina, being the State of São Paulo the biggest producer.

Taking into account that the proximity factor does not characterize the cluster formation in the nautical construction segment in Brazil, and also because it does not have anything similar in this segment as it has in the platform/UEP construction segment (PROMINP programme), it could be thought about implementing the cluster system like the one implemented in Holland. One or more leader companies of the nautical segment would be defined, and they could be responsible for integrating the other actors of the nautical segment with participation of the government, universities, research and development centres, technical schools, associations of all kinds, etc. PROMINP programme is led by Petrobras Company who is the agent to nationalize items for the construction of platform/UEP in Brazil, and to promote the development of the local industry.

In the nautical segment, the leader companies would have to play the same role, however, they would have to be more proactive and to integrate the greatest possible number of shipyards, suppliers of the supply chain, agencies, universities, research and development centres, the associations, etc.; to also focus on exportation, services and other specific niches that can be explored (Moura, 2008).

In the nautical construction segment, there is very little integration among shipyards and universities, practically isolated cases, when the complete segment, in Brazil, is studied. In what refers to the research and development centres, it is practically inexistent any type of integration among the main shipyards of this segment and the well-known centres in the country. When the specialized labour is analyzed, with competence and ability to act in this segment, it is noticed the total unpreparedness of the country, and that there isn’t so far universities or technical schools that enable the professionals for acting in this segment in Brazil (Moura, 2008; Moura; Botter, 2009).

In the nautical construction segment, few shipyards have some kind of partnership with the universities. It is necessary to increase this kind of partnership to promote the development of the sector and to make Brazil globally more competitive. There are products with quality, competitive costs, technology, however, with very small volume of production to supply the demand of some markets, such as the North American one.

Brazil does not possess anything of prominence that allows it to be recognized world-widely for developing high technology in the nautical construction segment, result of the partnership between shipyards and universities. With a few exceptions, there is a couple of suppliers of products to the nautical segment that stands out for having carried through the partnership between shipyard and university for the product development; however, they can be classified as isolated cases.

There is also the necessity of industrial policies which promote this partnership between shipyards, universities and research centres in Brazil.

The segment of nautical construction has potential markets like the European and North American ones. On the other hand, the shipyards have low production to supply these markets, specially the United States. It would be important a bigger integration between shipyards and universities for generation of research that would contributed for products and services development, promoting also, the growth of the supply chain of this sector, in the domestic territory. That way, Brazil could explore the world-wide parts and components market, besides of the nautical services.

In the naval construction segment, there is integration with the universities located in the South-eastern region of the country, predominating the States of São Paulo and Rio de Janeiro, however, this integration can still be bigger. Together with the construction of a new shipyard in the Northeast region of the country, it is searched to increase the integration with local universities; however, still, it is incipient and it does not demonstrate to be something that will promote research and development. Some advances have already happened in this segment of the Brazilian maritime industry, but, there is space available for much more integration. However, that very much depends on industrial policies that stimulate all the agents of the maritime industry for mobilizing themselves of reaching common objectives, benefiting all the set of related companies in direct or indirect way with the segment.

In the platform construction segment, there is this integration between universities and shipyards/EPC, but it must be better explored. The benefits generated still are punctual and small, knowing that the segment can be offered to all actors of the sector. This partnership should be increased so that Brazil could develop essential abilities in specific niches and gain market share.

This also could promote the growth of the economy, generating more employment and income distribution among the population and, increasing the entrance foreign currency, besides of the international recognition.

In the ship repair segment, the integration between university and shipyards is inexistent. In this segment, it would be important the integration between these two actors, because, world-widely, this market is very promising; and, Brazil could be structured to explore international markets that, nowadays, are dominated by Singapore and other countries that already appear among the great players, such as Dubai, in the United Arab Emirates.

References

ALTENBURG, T.; MEYER-STAMER, J. How to promote clusters: policy experiences from Latin America. World Development. vol. 27, no. 9, p.1693-1713, 1999.

AMATO NETO, J. Nets of Productive Cooperation and Regional clusters: opportunities to small and medium companies [Redes de Cooperação Produtiva e Clusters Regionais: oportunidades para as pequenas e médias empresas]. São Paulo: Atlas, 2000.

BABBIE, E. Methods of Survey Polls [Métodos de Pesquisa de Survey]. Belo Horizonte: Ed. UFMG, 2001.

BOTELHO, D.; ZOUAIN, D. M. (Org.). Quantitative research on Administration [Pesquisa Quantitativa em Administração]. São Paulo: Atlas, 2006.

Competitive Strategy – technique for the analysis of industries and competitors

COOPER, D.; SCHINDLER, P. Methods of research in administration [Métodos de Pesquisa em Administração]. 7. ed., Porto Alegre: Bookman, 2003.

COUTINHO, L. G., SABBATINI, R., RUAS, J. A. G.. Document: Acting Forces in the industry [Documento: forças atuantes na indústria]. NEIT-IE-Unicamp. PR-011 PROTRAN – Programa Tecnológico da Transpetro. Centro de Estudos em Gestão Naval. Escola Politécnica da Universidade de São Paulo, Departamento de Engenharia Naval e Oceânica, São Paulo, 2006.

DIJK, M. P. V.; SVERRISSON, A. Enterprise clusters in developing countries: mechanisms of transition and stagnation. Entrepreneurship & Regional Development, no. 15, p. 183-206, jul./sep., 2003.

DREJER, I.; KRISTENSEN, F. S.; LAURSEN K. Cluster studies as a basis for industrial policy: the case of Denmark. Industry and Innovation. ABI/INFORM Global, no. 6, dec.1999.

FLOYSAND, A.; JAKOBSEN, S. E. Clusters, social fields and capabilities: Rules and restructuring in Norwegian fish-processing clusters. Institute of Studies of Management & Organization. vol. 31, no. 4, p. 35-55, Winter 2001-2002.

GARCIA, R. External Economies and competitive advantages of producers in located systems of production: Marshall’s, Krugman’s and Porter’s visions [Economias externas e vantagens competitivas dos produtores em sistemas locais de produção: as visões de Marshall, Krugman e Porter]. Revista Ensaios Fundação de Economia e Estatística – Siegfried Emanuel Heuser, vol. 27, no. 2, p. 301-324, Porto Alegre, 2006.

GORDON, I. R.; MCCANN, P. Industrial clusters: complexes, agglomeration, and/or social networks? Urban Studies, vol. 37, no. 3, p. 513-532, 2000.

IGLIORI, D. C. Economy of industrial clusters and development [Economia dos Clusters Industriais e Desenvolvimento]. São Paulo: Iglu, 2001.

KRUGMAN, P. Development, geography and economic theory. Cambridge: MIT Press, 1995.

LAHNSTEIN, E. Development in the Norwegian maritime cluster. 1st European Maritime Cluster – Organisation Roundtable, Wassenaar, Netherlands, 26th and 27th April, 2004.

LANGEN, P. W. Clustering and performance: the case of maritime clustering in the Netherlands. Maritime Policy Management. vol. 29, no. 3, p. 209-221, 2002.

MACHADO, S. A. Dynamics of local productive arrangements: a case study in Santa Gertrudes, the new Brazilian pottery centre [Dinâmica dos arranjos produtivos locais: um estudo de caso em Santa Gertrudes, a nova capital da cerâmica brasileira]. Tese (Doutorado) – Escola Politécnica, Universidade de São Paulo, São Paulo, 2003.

MARSHALL, A. Principles of Economy [Princípios de Economia]. São Paulo: Nova Cultural, 2. ed., 1985.

MATTAR, F. N. Marketing research: Methodology and planning [Pesquisa de Marketing: metodologia – planejamento]. vol. 1 e 2, São Paulo: Atlas, 1999.

MAUCCI, G.; LUGO, E. E. Maritime clusters – the Panamanian case. International Association Of Maritime Economists - IAME, 2002.

MEYER-STAMER, J.; ALTENBURG, T. How to promote clusters: policy experience from Latin America. World Development, vol. 27, no. 9, p. 1693-1713, 1999.

MOURA, D. A. de. Analysis of the main segments of Brazilian Maritime Industry: a study on dimensions and critical success factors inherent to its competitiveness. Thesis (Ph.D.). Polytechnic School of the University of Sao Paulo. [Análise dos principais segmentos da indústria marítima brasileira: estudo das dimensões e dos fatores críticos de sucesso inerentes à sua competitividade]. Tese (Doutorado) – Escola Politécnica da Universidade de São Paulo, 2008).

MOURA, D. A., BOTTER, R. C. Are the Brazilian shipyards competitive in the segments of navy construction, platform construction/offshore, naval repair and yachting construction? 13th Congress International Maritime Association of Mediterranean, IMAM 2009, Istanbul, Turkey, 12-15 Oct. 2009, p 615-624.

NIJDAM, M. H.; LANGEN, P. W. Leader firms in the dutch maritime cluster. European Congress of the Regional Science Association – ERSA. 27th-30th, Finland, 2003.

PORTER, M. Clusters and the new economics of competition. Harvard Business Review. nov./dec., 1998.

____________. Estratégia competitiva – técnicas para análise de indústrias e da concorrência. 6. ed., Rio de Janeiro: Campus, 1991.

____________. On competition: Essential competitive strategies [Competição = on competition: estratégias competitivas essenciais]. Rio de Janeiro: Campus, 1999.

<http://www.gestaonaval.org.br/site/publicacoes.asp?cod2=11>. Access in: 29 march, 2007.

SCHMITZ, H. Does local co-operation matter? Evidence from industrial clusters in South Asia and latin America. Oxford Development Studies, vol. 28, no. 3, 2000.

SELLTIZ, C.; WRIGHTSMAN, L.; COOK, S. Research methods on social relations [Métodos de pesquisa nas relações sociais]. São Paulo: EPU, 1987.

SENNETT, J. Clusters, co-location and external sources of knowledge: the case of small instrumentation and control firms in the London region. Planning Practice & Research, vol. 16, no. 1, p. 21-37, 2001.

SIMMIE, J.; SENNETT, J. Innovative clusters: global and local linkages? National Institute Economic Review. ABI/INFORM Global, p. 87, oct. 1999.

SUZIGAN, W. et al. Identification, mapping

and structural characterization of productive

arrangements in Brazil [Identificação,

mapeamento e caracterização estrutural de

arranjos produtivos locais no Brasil]. Instituto

de Pesquisa Aplicada, out. 2006.

TUROK, I. Cities, clusters and creative industries:

the case of film and television in Scotland.

European Planning Studies, vol. 11, no. 5, jul.,

2003.

VIITANEN, M. et al. The finnish maritime cluster.

National Technology agency. Technology

Review 145, Helsinki, 2003.

WAITS, Mary J. The added value of the industry

cluster approach to economic analysis, strategy

development, and service delivery. Economic

Development Quarterly. vol. 14, feb. 2000.

WIJNOLST, N.; JENSSEN, J. I.; SODAL, S.

European Maritime Custers. global trends,

theoretical framework. the cases of Norway and

the Netherlands – policy recommendations.

Foundation Dutch Maritime Network. nov.

2003.